On Monday, March 17, 2026 (ET), the countdown to Lululemon’s results call is measured in small moments: a retail worker checking a phone during a break, an investor refreshing a brokerage screen, a longtime customer pausing over whether a familiar brand still feels “new. ” For Lulu Stock, the hours leading into the fourth-quarter and full-year 2025 results call have become less about a single number and more about a set of uncomfortable questions that won’t go away.

Those questions were sharpened earlier in the day by Chip Wilson, the founder of lululemon athletica inc. and one of the company’s largest shareholders, who issued a statement ahead of the call. In it, Wilson argued that shareholders should “critically” evaluate leadership’s claims of success or improvement and pressed the board and management for detailed answers about discounting, product “newness, ” operational mistakes, and persistent weakness in North America.

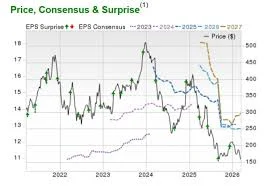

Separately, expectations for the coming report are already framed on Wall Street. Lululemon is set to report its Q4 earnings results on March 17 after the market closes (ET). Analysts are expecting earnings per share of $4. 78 on revenue of $3. 57 billion, compared with last year’s $6. 14 and $3. 61 billion. The company has beaten earnings in each of its last 16 quarters, but investors are focused on whether the slowdown is cyclical or structural—and whether an earnings beat alone can restore confidence.

What are investors watching for in Lulu Stock ahead of the Q4 earnings call?

Investors are watching for clear explanations of how lululemon plans to protect its premium brand while navigating discounting, refresh its product pipeline, and correct operational missteps—while also determining whether the company’s slowdown is cyclical or structural.

Wilson’s statement placed particular emphasis on what he described as a “disconnect” between the company’s creative engine and the board’s understanding of how brand power and product excellence drive “cultural strength, margin durability and long-term shareholder value. ” He urged leadership to provide “detailed answers” so that investors, partners, employees, and others “can understand where current leadership is taking this Company. ”

On the market side, analysts’ estimates—$4. 78 in earnings per share on $3. 57 billion in revenue—set a baseline for what a “normal” quarter might look like heading into the call. Yet even with a history of earnings beats, investors are weighing whether results can address deeper questions about momentum and relevance.

Why Chip Wilson is pressing the board on discounting, product creativity, and North America sales

Wilson’s critique focused on several interlocking themes. First: discounting. He asked how investors should reconcile messages about operational improvements with “continued discounting to offset declining North America store comps for which product was purchased. ” In his framing, discounting is not only a tactical decision but a strategic risk to brand power—he argued that “each dollar lost from discounting is a dollar that could have been invested into expanding the power of the lululemon brand. ”

Second: product and creativity. Wilson pointed to what he characterized as recent launches that look “stale and predictable, ” referencing language used by Interim Co-Chief Executive Officer Meghan Frank in an interview with. He pressed for clarity on how the board prioritizes “creativity and newness, ” what data informs launch decisions, and what changes have been made to oversight.

Third: execution errors. Wilson asked what structural changes have been made to address “increasing frequency of product failures, ” naming “Get Low” and “Breezethrough. ” He also asked whether the board has analyzed failures in new categories such as jeans, cosmetics, and running shoes—and whether shareholders will be told what the company learned.

Finally: North America as a bellwether. Wilson stated the company has reported negative or flat same store sales for the past seven consecutive quarters in North America, and he called for same store sales data in specific “trend-setting markets” including New York, Miami, Vancouver, and Los Angeles. His core concern: preventing underperformance in North America from translating to slower growth in mainland China and other international markets.

As a proposed response, he highlighted three independent candidates put forward in a campaign for change—Marc Maurer, Laura Gentile, and Eric Hirshberg—arguing they would ask tougher questions and bring stronger accountability and oversight.

Is the slowdown cyclical or structural—and what would settle the debate?

The looming question is whether lululemon’s slowdown reflects a cyclical hangover after years of strong growth or something more structural in consumer preference and competition. The cyclical argument points to tough comparisons after several strong years and a geographic shift in growth: international revenue rose 33% year-over-year and China Mainland sales climbed 46% in Q3, though those regions still account for about one-third of total revenue.

The structural argument, as described by some analysts, centers on intensifying competition in premium athleisure from newer rivals including Alo Yoga, Vuori, Athleta (GAP), and Nike. With apparel described as having very low switching costs and competitors investing heavily in influencer marketing aimed at younger consumers, the concern is that lululemon may be losing cultural momentum, particularly in the Americas.

In that context, a simple earnings beat may not be enough to lift sentiment. Investors are looking for “concrete evidence” the business can continue growing and remain relevant. Options pricing also reflects the tension: options traders are expecting a 10. 5% move in either direction immediately after the earnings report.

What happens next after earnings—and what the market may demand

Heading into the call later on March 17 (ET), Lulu Stock sits between two forms of accountability: the near-term scoreboard of earnings and the longer-term test of brand power. Analysts currently hold a Hold consensus rating on LULU stock based on one Buy, 17 Holds, and zero Sells assigned in the past three months, with an average price target of $202. 87 per share implying 26. 9% upside potential.

But the human reality beneath those ratings is more basic: people want to know whether the product still feels worth waiting for, whether the company can grow without leaning on discounting, and whether mistakes are being fixed in ways that will prevent repeats. Wilson’s statement framed the day as a demand for specificity—how decisions are made, what has changed, and how leadership understands the link between creativity, product excellence, and durable value.

By the time the market closes and the numbers arrive, the scene will look familiar: screens glowing, conference-call audio, a few sentences that move the stock or fail to. The difference is what comes after. If the company’s answers clarify strategy on discounting, product “newness, ” and North America performance, Lulu Stock may find firmer ground. If not, the same questions will return—louder—at the next call.